Inovance isn't a name you'll hear in most casual conversations about tech, but it should be. While everyone's obsessing over the latest Silicon Valley software updates, this Shenzhen giant is quietly moving to dominate the physical world. By filing for a Hong Kong IPO that could raise upwards of $2 billion, Shenzhen Inovance Technology is signaling that it's ready to take its fight with global titans like ABB and Fanuc to a much larger stage.

If you're an investor or just someone watching the automation space, ignore this listing at your own peril. This isn't just another Chinese company looking for a quick cash grab. It's a strategic pivot. They're already the king of the hill in China’s domestic industrial automation market. Now, they’re coming for the rest of the world.

The Local Hero with Global Ambitions

Inovance has spent years building a fortress in China. Most people don't realize how hard it is to beat established Japanese and European brands on their home turf, but Inovance did exactly that. They started with low-voltage inverters and quickly expanded into servo systems, PLC controllers, and industrial robots.

They’re currently the top domestic brand for servo systems in China, often outperforming international competitors on both price and localized service. In 2024, the company reported revenue of $5.2 billion, a 22% jump year-over-year. That’s not a fluke; it’s the result of a relentless focus on R&D, which usually eats up nearly 10% of their annual revenue.

By listing in Hong Kong, they're looking to solve a specific problem: global perception and capital access. Operating as an A-share company in Shenzhen is great for local growth, but an H-share listing provides the "hard currency" and international visibility needed to acquire foreign targets and build out global supply chains.

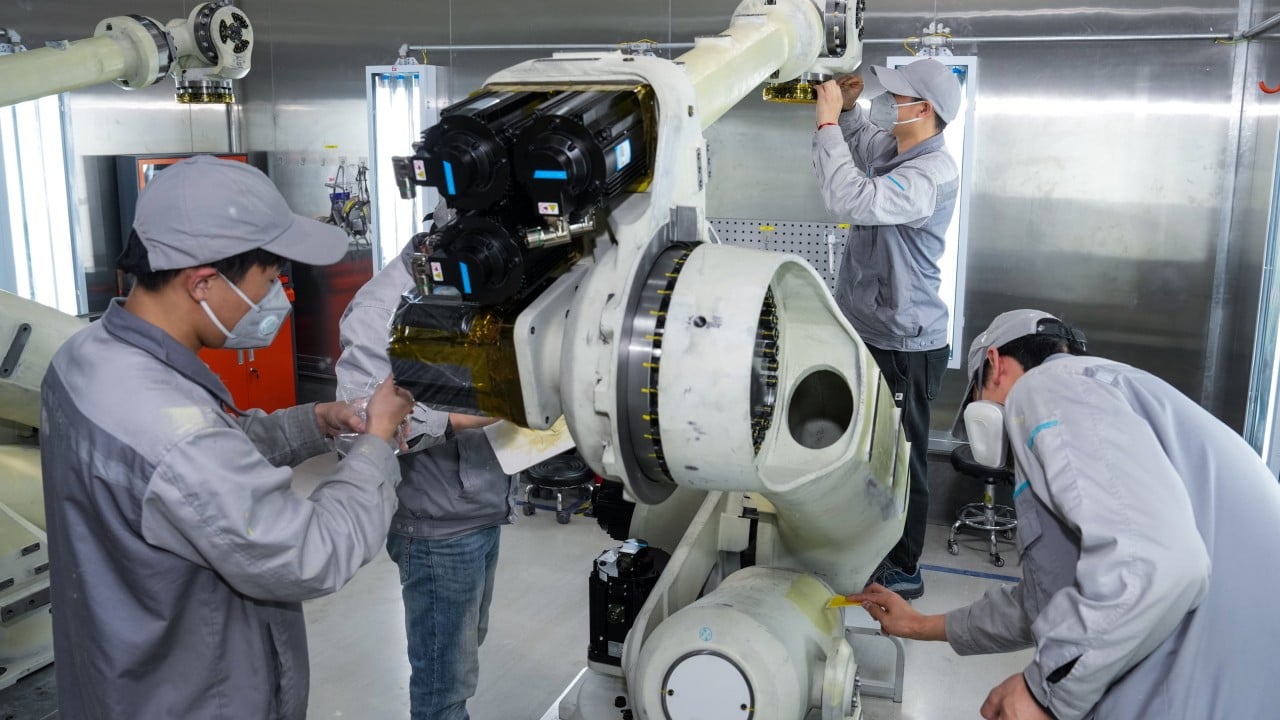

Breaking the Robot Ceiling

The industrial robot market is notoriously difficult to crack. It's a game of precision, reliability, and long-term trust. For decades, the "Big Four"—ABB, Fanuc, Kuka, and Yaskawa—held a virtual monopoly. Inovance is the first Chinese firm that actually looks like it could join that inner circle.

Why is this happening now? China is currently going through a massive automation push to counter its shrinking workforce and rising labor costs. In early 2026, Chinese industrial robot production surged by over 30%. Inovance is the primary beneficiary of this trend. They aren't just selling "cheap" robots anymore. They're selling integrated systems that handle everything from New Energy Vehicle (NEV) production lines to high-end electronics assembly.

The NEV Factor

You can't talk about Inovance without talking about electric vehicles. They’ve tied their wagon to the NEV star, providing motor controllers and power systems to some of the biggest names in the industry. While the NEV market has seen some price wars and margin pressure lately, Inovance has managed to keep its head above water by diversifying into general industrial automation.

Their 2025 performance showed a 25% revenue increase in the third quarter alone. That kind of growth in a cooling economy is rare. It tells us that even when the broader market struggles, the "smart manufacturing" sector is still getting funded. Manufacturers have realized that if they don't automate, they won't survive the next decade.

Why Hong Kong Matters Right Now

The Hong Kong IPO market has been having a bit of a renaissance in early 2026. After a few dry years, we’re seeing a flood of "A+H" listings—companies already listed in Mainland China seeking a secondary home in Hong Kong. In the first quarter of 2026, Hong Kong raised nearly $110 billion HKD, its best start in five years.

Inovance is hitting the market at the perfect time. Investors are hungry for "hard tech" and companies with real earnings, not just "AI-adjacent" hype. They want firms that make things you can drop on your foot.

What to watch for in the prospectus

- Overseas Revenue Growth: Look at how much of their money comes from outside China. If that percentage is growing, it means their "globalization" strategy is actually working.

- Margin Stability: With intense price competition in the robot sector, check if they can keep their net profit margins in the 13-15% range.

- R&D Allocation: Are they still spending heavily on next-gen tech like collaborative robots (cobots) and humanoid components?

The Humanoid Hype vs. Reality

There’s a lot of talk about Inovance moving into humanoid robots. While it's a sexy topic that drives stock prices, the real money for the next three years is still in "boring" industrial arms and servo motors. Inovance is smart enough to play both sides. They’re developing the high-precision actuators and sensors needed for humanoids, but they aren't betting the farm on them yet.

They're basically selling the shovels for the humanoid gold rush. Whether the robots end up looking like people or just better versions of current factory arms, Inovance wins because they own the underlying tech stack.

Getting Skin in the Game

If you're looking to play the long-term trend of global automation, this IPO is a major entry point. It represents the transition of Chinese manufacturing from "made in China" to "engineered by China."

Don't wait for the mainstream financial media to catch up. Start digging into their Shenzhen filings (ticker 300124) now to see the raw data before the Hong Kong prospectus hits the shelves. If they can replicate even half of their domestic success on a global scale, the current valuation of around $26 billion will look like a bargain. Watch the price determination dates closely in late April—this is where the institutional sentiment will truly reveal itself.